Recently, the Internal Revenue Service (IRS) announced (See Revenue Procedure 2023-23) cost-of-living adjustments to the applicable dollar limits for health savings accounts (HSAs), high-deductible health plans (HDHPs) and excepted benefit health reimbursement arrangements (HRAs) for 2024. All of the dollar limits currently in effect for 2023 will change for 2024, with the exception of one limit. The HSA catch-up contribution for individuals ages 55 and older will not change as it is not subject to cost-of-living adjustments.

The Biden administration originally announced its intent to end the COVID-19 National Emergency (NE) and the COVID-19 Public Health Emergency (PHE) on May 11, 2023 (read our prior article for more information). Although the end date of the NE was subsequently advanced to April 10, 2023, by Congressional resolution, the US Departments of Labor, Health and Human Services, and the Treasury (the Departments) have given no indication that the change will affect employee benefits plans. Plan sponsors should continue to treat May 11 as the end of the NE until the Departments say otherwise.

During the COVID-19 pandemic, certain permissive practices were allowed by high-deductible health plans (HDHPs) and health savings accounts (HSAs). This article explores whether these benefit offerings can be continued at the end of the PHE and NE.

HDHPs AND HSAs

IRS Notice 2020-15 temporarily permits the coverage of COVID-19 testing with no cost-sharing for HDHPs. It provides that an HDHP will not fail to be an HDHP merely because the plan covers expenses related to COVID-19 testing and treatment prior to satisfying the applicable minimum deductible. This guidance was not directly tied to the NE or the PHE, meaning that it will eventually lapse. The eighth question/answer of the FAQs indicates that individuals covered by an HDHP who have purchased items related to COVID-19 testing or treatment prior to meeting the applicable minimum deductible can continue to contribute to an HSA until further guidance is issued. The Departments also assured plan sponsors that future changes will generally not require HDHPs to make mid-year changes for covered individuals to remain eligible to contribute to an HSA.

Thus, individuals covered by an HDHP may continue to contribute to an HSA following the end of the PHE. COVID-19 vaccinations also continue to be considered preventive care under Section 223 of the Code for purposes of determining whether a health plan is an HDHP.

ACTION ITEMS

Once the PHE and NE have ended, employers can continue their practice of allowing individuals covered by an HDHP plan to contribute to an HSA. Employers need to also consider whether they will continue to cover COVID-19 tests as required by a doctor or OTC without cost-sharing. Employers should strategize what effect this might have on the HDHP. This might also require an amendment to the health plan or its summary plan description. Employers should continue to watch for further guidance from the Departments on this issue.

The Biden administration has announced its intention to end the COVID-19 National Emergency (NE) and the COVID-19 Public Health Emergency (PHE) on May 11, 2023 (read our series introduction for more information).

On March 29, 2023, the US Departments of Labor, Health and Human Services, and Treasury (the Departments) issued a set of Frequently Asked Questions (available here), which answered questions from stakeholders relating to the various laws, regulations and other guidance enacted or adopted in connection with the NE and PHE. The FAQs include eight questions related to the anticipated end of the “Outbreak Period” on July 10, 2023, which is 60 days after the end of the NE and PHE on May 11 (rules regarding the Outbreak Period are set forth in our earlier articles here and here). Below are the highlights:

Following the end of the PHE, plans and issuers can impose cost-sharing, prior authorization or other medical management requirements for COVID-19 diagnostic tests, although the Departments encourage plans not to do so.

Plans and issuers are encouraged to notify plan participants of changes regarding COVID-19 diagnosis, testing and treatment. Special rules apply under which Summaries of Benefits and Coverage (SBCs) need not be amended mid-year.

While plans and issuers will no longer be required to post prices for diagnostic tests furnished after May 11, they are nevertheless encouraged to do so.

Plans must continue to cover vaccines that qualify as preventive services, without cost-sharing, when provided in-network.

The FAQs provide examples relating to the application and termination of extended time periods for elections under the Consolidated Omnibus Budget Reconciliation Act (COBRA) and the Health Insurance Portability and Accountability Act (HIPAA).

In what is a welcome surprise, the FAQs confirm that individuals covered by a High-Deductible Health Plan (HDHP) will remain Health Savings Account (HSA)-eligible until further notice even if the HDHP in which they are enrolled provides medical care services and items purchased related to testing for and treatment of COVID-19 prior to the satisfaction of the HDHP’s applicable minimum deductible.

To keep employers apprised of the rules and to assist with providing notice to plan participants of the changes that will accompany the end of the NE and PHE, the Department of Labor has issued two blog posts, which are available here and here.

Action Items: We urge plan sponsors to pay particular attention to notifying employees of the upcoming changes that will accompany the end of the PHE and NE and to ensure that participants covered under an HDHP understand that they may continue to contribute to their HSAs. Employers should consider communicating these changes to their employees.

For any questions regarding the end of the PHE and/or NE, please contact your regular McDermott lawyer or one of the authors.

The Biden administration has announced its intent to end the COVID-19 National Emergency (NE) and the COVID-19 Public Health Emergency (PHE) on May 11, 2023 (read our prior article for more information). In response to the COVID-19 pandemic, lawmakers and agencies made legislative and regulatory changes to expand access to telehealth services for individuals. This article explores what will happen to these temporary telehealth benefits at the end of the PHE and NE.

Current flexibilities under the Affordable Care Act (ACA) allow applicable large employers (ALEs) to offer stand-alone telehealth and remote care services to employees who were not eligible for other employer coverage during the PHE.

In addition, the Coronavirus Aid, Relief, and Economic Security Act (CARES) Act and IRS Notice 2020-29 established a temporary telehealth safe harbor, providing that a high-deductible health plan (HDHP) could cover telehealth and other remote care services on a pre-deductible basis without impacting an individual’s ability to contribute to an HSA. This relief applied to services provided on or after January 1, 2020, with respect to plan years beginning on or before December 31, 2021. Thus, for most calendar-year plans, this relief ended on December 31, 2021. The Consolidated Appropriations Act, 2022 (CAA 2022) renewed the relief under the CARES Act for months beginning after March 31, 2022, and before January 1, 2023—but it created a three-month gap in coverage from January 1, 2022, to March 31, 2022. The CAA 2022 also extended certain flexibilities related to Medicare coverage and payment for telehealth services through the end of 2024. The relief provided under the CAA 2022, however, was provided on a temporary basis and not tied to the PHE or NE.

Effective December 29, 2022, the Consolidated Appropriations Act, 2023 (CAA 2023) provided a two-year extension allowing first-dollar coverage of telehealth under an HDHP so that individuals can access services without needing to meet a deductible first. The CAA 2023 extends telehealth relief for plan years beginning after December 31, 2022, and before January 1, 2025. Most calendar year plans should therefore have coverage of pre-deductible telehealth services without affecting HSA eligibility for all of 2023 and 2024. When the PHE ends, stand-alone telehealth offerings must cease, but telehealth offerings on a pre-deductible basis can continue.

The stand-alone telehealth relief under the ACA is available until the end of the latest plan year that begins on or before the last day of the PHE. For calendar-year plans, this relief would last until December 31, 2023. When an employer ends its stand-alone telehealth benefit, it may need to provide participants a 60-day notice of a material reduction in benefits.

Employers offering telehealth coverage on a pre-deductible basis with HDHPs have been provided statutory relief through December 31, 2024, through the CAA 2023. However, employers should continue to watch for legislative updates regarding telehealth. Lawmakers have proposed multiple other bills in Congress to extend or make permanent telehealth flexibilities.

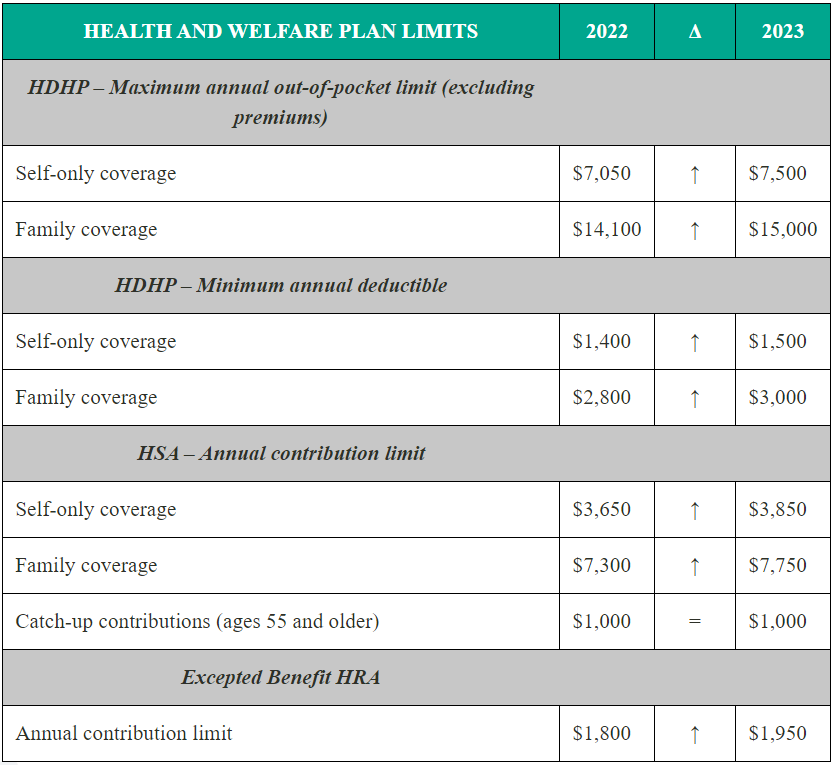

Recently, the Internal Revenue Service (IRS) announced (See Revenue Procedure 2022-24) cost-of-living adjustments to the applicable dollar limits for health savings accounts (HSAs), high-deductible health plans (HDHPs) and excepted benefit health reimbursement arrangements (HRAs) for 2023. All of the dollar limits currently in effect for 2022 will change for 2023, with the exception of one limit. The HSA catch-up contribution for individuals ages 55 and older will not change as it is not subject to cost-of-living adjustments.

The table below compares the applicable dollar limits for HSAs, HDHPs and excepted benefit HRAs for 2022 and 2023.

NEXT STEPS

Plan sponsors should update payroll and plan administration systems for the 2023 cost-of-living adjustments and incorporate the new limits in relevant participant communications, such as open enrollment and communication materials, plan documents and summary plan descriptions.

For further information about applying the new HSA, HDHP and excepted benefit HRA plan limits for 2023, please contact your regular McDermott lawyer or one of the authors below.

The Internal Revenue Service (IRS) recently announced the cost-of-living adjustments to the applicable dollar limits for various employer-sponsored retirement and welfare plans for 2022. Most of the dollar limits currently in effect for 2021 will increase.

The Internal Revenue Service recently announced cost-of-living adjustments to the applicable dollar limits for health savings accounts, high-deductible health plans and excepted benefit health reimbursement arrangements for 2022. Some of the dollar limits currently in effect for 2021 will change for 2022.

The Internal Revenue Service (IRS) recently announced the cost-of-living adjustments to the applicable dollar limits for various employer-sponsored retirement and welfare plans for 2021. Nearly all of the dollar limits currently in effect for 2020 will remain the same, with only a few amounts experiencing minor increases for 2021.

Prior to the pandemic, ultra-low unemployment at roughly 3.3% put a spotlight on ‘lifestyle benefits’ for employees such as gym memberships and pet sitting. When the COVID-19 crisis hit, the focus immediately shifted for many plan sponsors.

Some employers are now offering high-deductible health plans (HDHPs) paired with health savings accounts (HSAs). Scaling back on company matches to 401(k) plans and contributions to profit sharing accounts are two other areas where employers are trying to save money, said Lisa Loesel, an employee benefits partner at McDermott.

“Depending on what kind of plan they have and the terms set forth for them, we have seen plan sponsors delay the timing of their contributions, change the amount, move from a fixed to a discretionary amount or even cut their contributions indefinitely,” Loesel said in a recent article for PLANSPONSOR Magazine.

Among sponsors offering a pension plan, more are de-risking their plans. “The market happens to be favorable for doing this right now,” she says.

To help cafeteria plan participants address challenges arising from the COVID-19 crisis, the Internal Revenue Service recently issued guidance allowing employers to make a number of participant-friendly changes under their cafeteria plans. While employer adoption of these more flexible rules is voluntary, plan sponsors should work with third-party administrators, insurance providers and legal advisors to ensure that the new provisions are properly adopted, documented and communicated.

Subscribe

Subscribe

Law")