The US Securities and Exchange Commission (SEC) recently approved amendments to clawback policy listing standards proposed by the New York Stock Exchange (NYSE) and the Nasdaq Stock Market LLC (Nasdaq) that extend the effective date of the exchanges’ respective listing standards to October 2, 2023. Issuers listed on the NYSE and Nasdaq now have until December 1, 2023 (60 days from the new effective date) to comply with their respective exchange’s listing standards.

The new compliance focus on executive compensation, as announced by the US Department of Justice (DOJ) on March 3, 2023, has significant implications for how healthcare organizations address both corporate compliance and compensation programs for their executives. It also raises new issues for the board of directors’ oversight of compliance and compensation functions.

In a recent webinar, McDermott’s Ralph E. DeJong, Michael W. Peregrine, Sarah E. Walters and Eugene I. Goldman discussed the new policies, possible responses by management and boards, and potential strategies for responding to the policy goals of the DOJ and the Delaware Chancery Court.

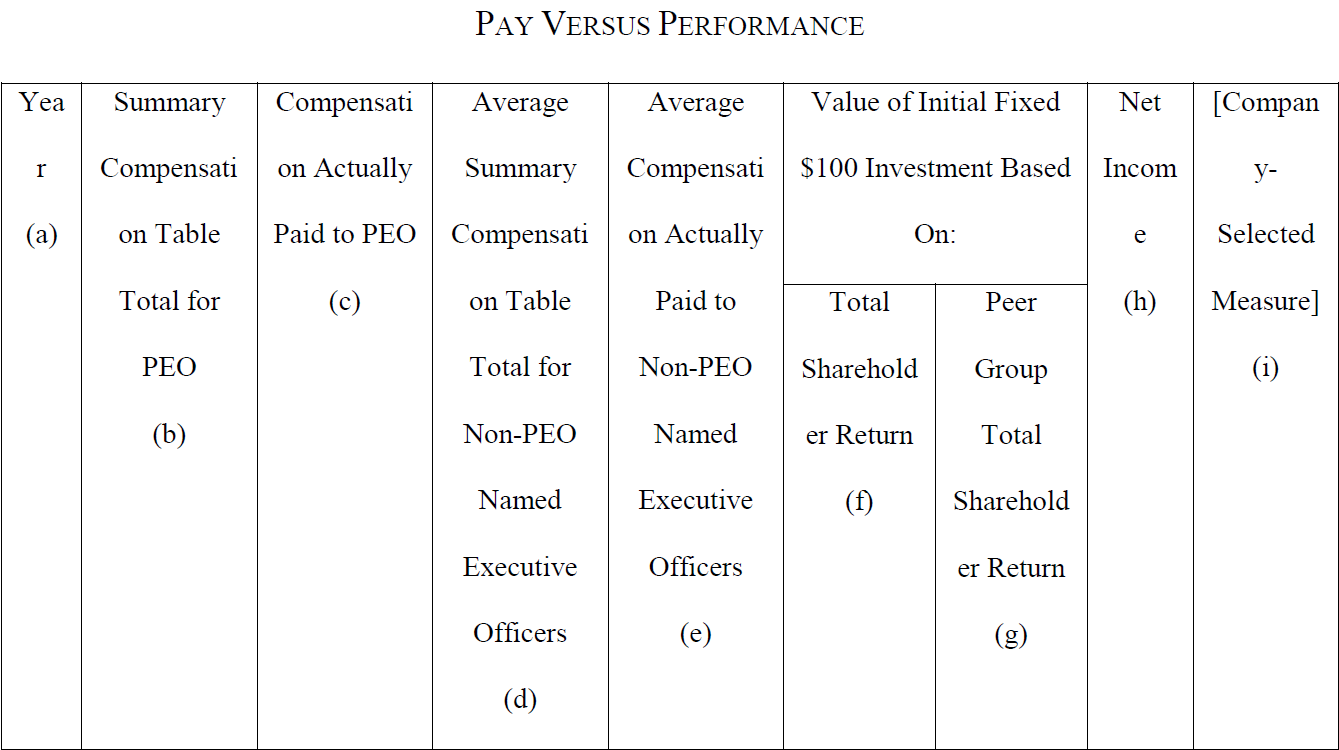

On August 25, 2022, the US Securities and Exchange Commission (SEC) adopted final rules imposing new mandatory “pay for performance” disclosures for most public companies (foreign private issuers, emerging growth companies and registered investment companies are excluded). These rules implement Section 953(a) of the Dodd-Frank Act, which provided for the SEC to adopt pay for performance rules requiring disclosure in a “clear manner” of the relationship between executive compensation “actually paid” and the company’s “financial performance” taking into account changes in stock value, dividends and distributions.

The final rules, which are primarily set forth in Item 402(v) of Regulation S-K, impose the following new tabular disclosure for any proxy statement or information statement for which executive compensation under Item 402 is required:

Important aspects of this table include the following:

Compensation “actually paid” to both the principal executive officer (PEO) (a/k/a CEO) and, as a group, the other named executive officers in the annual proxy statement, which is a measure that will require calculations different than amounts reported in the Summary Compensation Table, particularly for equity awards and pension benefits.

Financial performance is to be disclosed with respect to total stockholder return (TSR) for the company, its peer group and net income.

A public company covered by these rules can choose to use either the peer group used for its 10-K disclosures (under Item 201(d)) or the custom peer group in its CD&A for this table.

Issuers will be required to identify a “company selected measure” specific to their businesses (other than TSR and net income) that represents the “most important” financial performance measure used to link compensation actually paid to company financial performance.

The information required by the table is required to cover the five most recently completed fiscal years subject to a transition phase-in rule for 2023 and 2024.

Public companies will also need to provide a clear description of the relationship between each of the financial performance measures in the table and the executive compensation actually paid to its CEO and, on average, its other named executive officers during the lookback period, as well as the relationship between its TSR and the TSR of its peer group.

In addition, public companies will also need to identify the three to seven financial performance measures (or, in some cases, certain non-financial measures) that it determines are its most important measures.

Smaller reporting companies may avail themselves of scaled-back disclosure under Item 402(v), including a shorter lookback period (three years instead of five years) and no requirement to include a custom peer group, a tabular list or a company-selected measure.

Complying with these rules will require changes to existing forms of proxy disclosure. The extent to which these disclosures impact the amount or [...]

The US Department of Labor (DOL) recently issued guidance for the first time on the investment of retirement plan assets in cryptocurrencies. Compliance Assistance Release No. 2022-01 cautions 401(k) plan fiduciaries to “exercise extreme care” before allowing participants to invest plan assets in cryptocurrencies because cryptocurrencies “present significant risks and challenges to participants’ retirement accounts, including significant risks of fraud, theft, and loss.” In this Intellectual Property & Technology Law Journal article, McDermott Partners Andrea S. Kramer and Brian J. Tiemann outline what retirement plan fiduciaries need to know about cryptocurrency investments in the current market.

As the popularity of cryptocurrency continues to grow, what do employee benefits lawyers need to know about this emerging investment option? McDermott Partners Andrew Liazos, Andrea Kramer and Brian Tiemann recently offered their perspectives about cryptocurrencies and how they relate to Employee Retirement Income Security Act of 1974 (ERISA) plans, individual retirement accounts (IRAs) and incentive awards in an American Bar Association virtual event.

As cryptocurrencies gain popularity, employers are considering how they can be used as part of compensation arrangements and benefit plans to attract and retain talent. McDermott Partners Andrew Liazos, Andrea Kramer and Brian Tiemann recently offered their perspectives about cryptocurrency, Internal Revenue Service (IRS) taxation guidance of convertible virtual currencies and other cryptocurrency-related compensation issues in an American Bar Association virtual event.

Long considered controversial from economic and shareholder perspectives, living wage concepts are receiving more attention in the context of economic policy, social responsibility and ESG investing. As progressive perspectives concerning income equality, and executive and employee compensation, are becoming more mainstream, corporate leaders should prepare for greater engagement in this important conversation.

In June, the US Department of Labor issued an information letter indicating that it will allow defined contribution retirement plans (such as 401(k) plans) to indirectly invest in private equity funds. While information letters are not binding, this new guidance creates a significant opportunity for plan sponsors to consider investment options that include private equity funds. However, it will be important for both plan sponsors and funds to carefully evaluate potential investments for compliance with fiduciary requirements.

Corporations looking to use partnerships to avoid the executive compensation deduction limitation may be out of luck. The new proposed regs (REG-122180-18) on the section 162(m) executive compensation deduction limitation include a rule on compensation paid by a partnership to an executive of a publicly held corporation that’s subject to the limitation.

McDermott’s Andrew C. Liazos contributes to a Tax Notes article that takes a look at these new regulations and what they mean for partnership arrangements.

During the previous quarter, the SEC acted to expand the number of companies that may rely on the “smaller reporting company” scaled disclosure regime and Congress directed revisions to the Regulation A+ and Rule 701 exemptions. The SEC also took enforcement action on a major cybersecurity breach, reinforcing its recent interpretive guidance on the subject. The director of the SEC Division of Corporation Finance also spoke on how blockchain assets may or may not constitute securities, and the 9th Circuit created a circuit split related to securities litigation after a tender offer.

Subscribe

Subscribe

Law")