A recent US Court of Appeals for the Seventh Circuit case supplies answers to many questions left open in 401(k) fee litigation cases after the US Supreme Court’s ruling earlier this year in Hughes v. Northwestern University. Specifically, to survive a motion to dismiss in the Seventh Circuit, the recent ruling in Albert v. Oshkosh Corp. reiterated that plaintiffs must allege both high fees and substandard services or performance in comparison to other similar 401(k) plans.

The Internal Revenue Service (IRS) recently issued needed relief to extend some amendment deadlines for non-governmental qualified retirement plans and 403(b) plans, and for individual retirement accounts (IRAs) under the Setting Every Community Up for Retirement Enhancement Act of 2019 (SECURE Act), the Bipartisan American Miners Act of 2019 (Miners Act), and certain provisions of the Coronavirus Aid, Relief, and Economic Security Act (CARES Act) until December 31, 2025. However, the IRS did not provide relief for all required amendments for the 2022 plan year. Plan sponsors that elected to offer COVID-related distributions or loan relief (or utilized disaster-related relief for loans or distributions under the Taxpayer Certainty and Disaster Tax Relief Act of 2020) still need to amend their plans by the end of 2022 plan year.

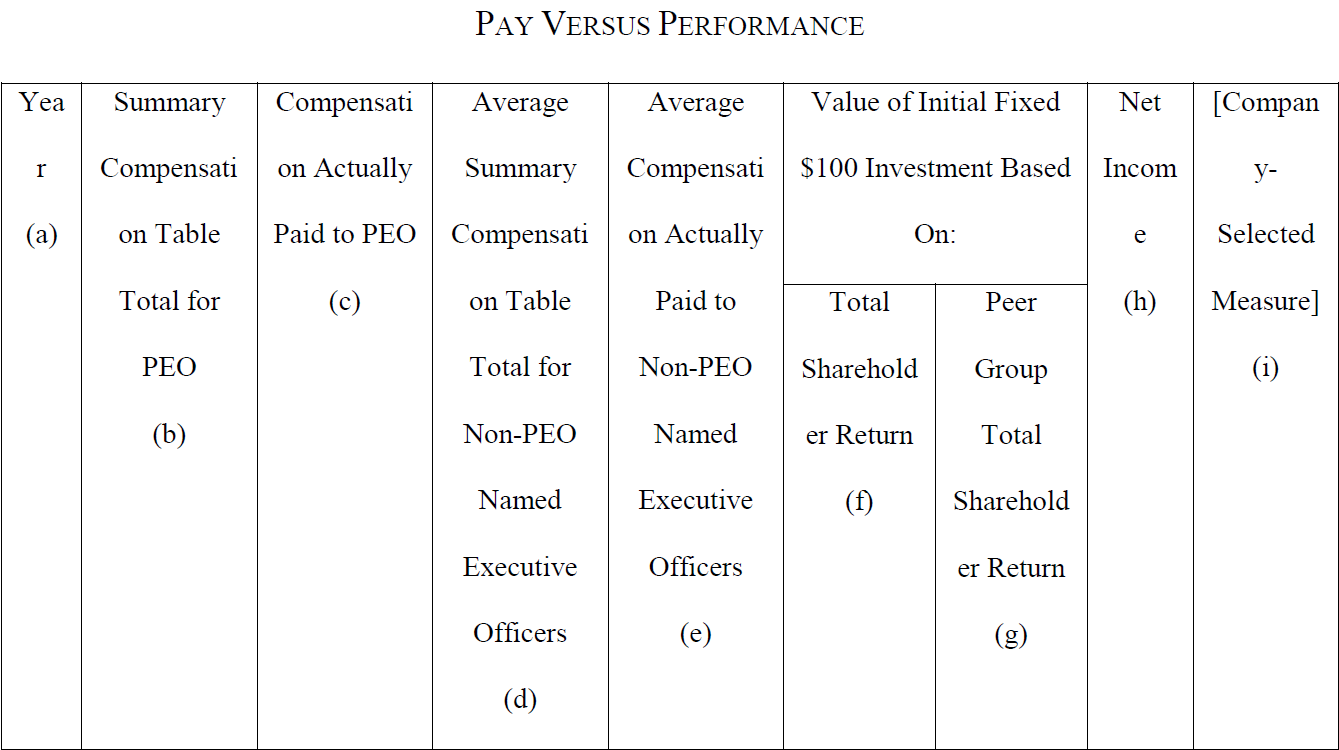

On August 25, 2022, the US Securities and Exchange Commission (SEC) adopted final rules to implement the pay versus performance disclosure requirement mandated by the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act). The Dodd-Frank Act added Section 14(i) to the Securities Exchange Act of 1934, which directs the SEC to adopt rules that require registrants to clearly disclose the relationship between executive compensation actually paid and the registrant’s financial performance. More than 12 years after US Congress passed the Dodd-Frank Act, the SEC has adopted Item 402(v) of Regulation S-K to put these disclosure requirements into effect in time for the 2023 proxy season.

On August 25, 2022, the US Securities and Exchange Commission (SEC) adopted final rules imposing new mandatory “pay for performance” disclosures for most public companies (foreign private issuers, emerging growth companies and registered investment companies are excluded). These rules implement Section 953(a) of the Dodd-Frank Act, which provided for the SEC to adopt pay for performance rules requiring disclosure in a “clear manner” of the relationship between executive compensation “actually paid” and the company’s “financial performance” taking into account changes in stock value, dividends and distributions.

The final rules, which are primarily set forth in Item 402(v) of Regulation S-K, impose the following new tabular disclosure for any proxy statement or information statement for which executive compensation under Item 402 is required:

Important aspects of this table include the following:

Compensation “actually paid” to both the principal executive officer (PEO) (a/k/a CEO) and, as a group, the other named executive officers in the annual proxy statement, which is a measure that will require calculations different than amounts reported in the Summary Compensation Table, particularly for equity awards and pension benefits.

Financial performance is to be disclosed with respect to total stockholder return (TSR) for the company, its peer group and net income.

A public company covered by these rules can choose to use either the peer group used for its 10-K disclosures (under Item 201(d)) or the custom peer group in its CD&A for this table.

Issuers will be required to identify a “company selected measure” specific to their businesses (other than TSR and net income) that represents the “most important” financial performance measure used to link compensation actually paid to company financial performance.

The information required by the table is required to cover the five most recently completed fiscal years subject to a transition phase-in rule for 2023 and 2024.

Public companies will also need to provide a clear description of the relationship between each of the financial performance measures in the table and the executive compensation actually paid to its CEO and, on average, its other named executive officers during the lookback period, as well as the relationship between its TSR and the TSR of its peer group.

In addition, public companies will also need to identify the three to seven financial performance measures (or, in some cases, certain non-financial measures) that it determines are its most important measures.

Smaller reporting companies may avail themselves of scaled-back disclosure under Item 402(v), including a shorter lookback period (three years instead of five years) and no requirement to include a custom peer group, a tabular list or a company-selected measure.

Complying with these rules will require changes to existing forms of proxy disclosure. The extent to which these disclosures impact the amount or [...]

How can organizations cope with change fatigue in uncertain times? In this Forbes article, McDermott Partner Michael Peregrine draws on historical and present examples to argue that effective leadership starts with the proper tone at the top.

“A positive organizational culture may come less easily these days, not because the organization itself is less robust, but because of the insidious impact of change fatigue,” Peregrine writes. “And that fatigue can undermine the spirit of the workforce and its faith in the future.”

Last month, the Washington Court of Appeals affirmed a lower court’s decision to dismiss a challenge to the recently enacted payroll expense tax in Seattle, WA. Seattle Metro. Chamber of Commerce v. City of Seattle, No. 82830-4-I, 2022 WL 2206828 (Wash. Ct. App. June 21, 2022).

The tax, which went into effect on January 1, 2021, applies to entities “engaging in business within Seattle” and is measured using the business’s “payroll expense” (defined as “compensation paid in Seattle to employees,” including wages, commissions, salaries, stock, grants, gifts, bonuses and stipends). The tax only applies to businesses with a payroll expense of more than $7 million in the prior calendar year, and compensation is considered “paid in Seattle” if the employee works more than 50% of the time in the city.

On May 5, 2022, McDermott Partner Erin Turley delivered a presentation during the 2022 TEA National Conference titled “Understanding a Trustee’s Role in Management Incentive Plans.” Her presentation focused on the trustee’s role in Management Incentive Plans (MIPs), how retention and performance stock appreciation rights (SARs) impact an employee stock ownership plan (ESOP) and ways to avoid trustee pitfalls with a MIP. Erin also discussed types of synthetic equity design decisions, incentive stock options, non-statutory stock options and phantom stock/SARs.

The presentation concluded with the following fiduciary considerations:

Since the issuance of any equity or synthetic equity can have a potentially dilutive impact on the ESOP, it is important for any plan to be in the best interest of the ESOP plan participants.

As a result, one of the primary objectives of the plan should be to identify and select a group of people to be incentivized and rewarded to drive value for everybody.

For example, in the case of a SAR, you are rewarding a group of individuals based only on appreciation in the value of the company stock. If the value goes up, that’s good for everybody.

The overall compensation program should be in line with compensation practices for comparable-type positions in the industry, perhaps taking geography into account.

While the United States awaits the Supreme Court’s ruling in Dobbs v. Jackson, which may overturn Roe v. Wade and eliminate the federal standard for abortion access, some states are considering setting their own standards that would ban or protect the medical procedure. This state-by-state rulemaking will cause some difficulty for employer plans, and employers are increasingly exploring ways to continue providing abortion coverage.

On January 15, 2022, the New York City Council enacted Local Law 32 of 2022 (Wage Transparency Law or Law) to amend the New York City Human Rights Law (NYCHRL) to require that most employers include compensation data in their job advertisements. The Law was supposed to take effect on May 15, 2022, however, it faced criticism over a number of ambiguities, including undefined penalties. In response, on April 28, 2022, the New York City Council passed an amendment to the Wage Transparency Law. Among the biggest changes is that employers now have until November 1, 2022—more than six months—to ensure compliance with the Law’s requirements. If Mayor Eric Adams signs the Law, which he is expected to do, New York City will become the second jurisdiction in the country (the first being Colorado) to require employers to include minimum and maximum potential salary amounts for open positions in job postings.

Earlier this spring, McDermott Partner Erin Turley delivered a presentation about the impacts of recent Employee Retirement Income Security Act of 1974 (ERISA) litigation. Lawsuits now target both large and small employee benefit plans; plan sponsors are being sued and dragged into complex and lengthy litigation, thus changing the basic economics of the provision of fiduciary liability insurance. In response to these lawsuits, plan sponsors are looking to outsource as much of this fiduciary responsibility and potential liability and exposure as possible.

Subscribe

Subscribe

Law")