Subscribe

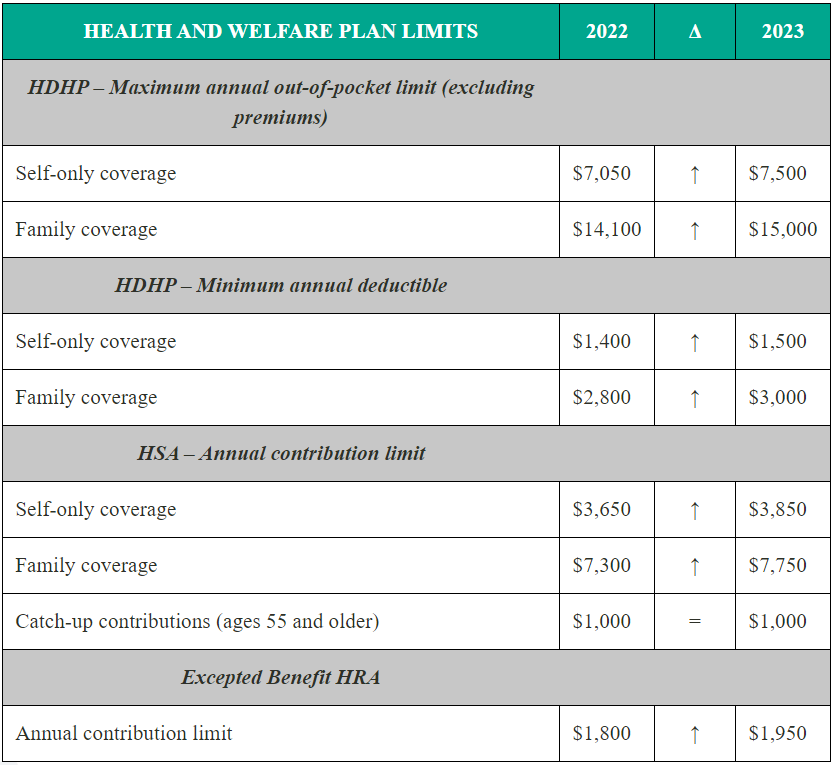

SubscribeThe Internal Revenue Service (IRS) recently announced (see Revenue Procedure 2024-25) cost-of-living adjustments to the applicable dollar limits for health savings accounts (HSAs), high-deductible health plans (HDHPs) and excepted benefit health reimbursement arrangements (HRAs) for 2025. All of the dollar limits currently in effect for 2024 will change for 2025, with the exception of one limit. The HSA catch-up contribution for individuals ages 55 and older will not change as it is not subject to cost-of-living adjustments.

read more

")

Law")